Why are cash flow problems in business such a big deal right now?

Running a small business has never been a walk in the park — but the last couple of years have been something else.

Rising costs, tax pressures and squeezed margins have combined to create a real headache for UK SMEs. Lovey surveyed 504 UK small business owners to understand how they're coping, and what's driving them towards SME lending in 2026.

The findings paint a clear picture: cash flow problems in business aren't just a minor inconvenience — they're costing owners real opportunities.

Download the full SME Outlook report

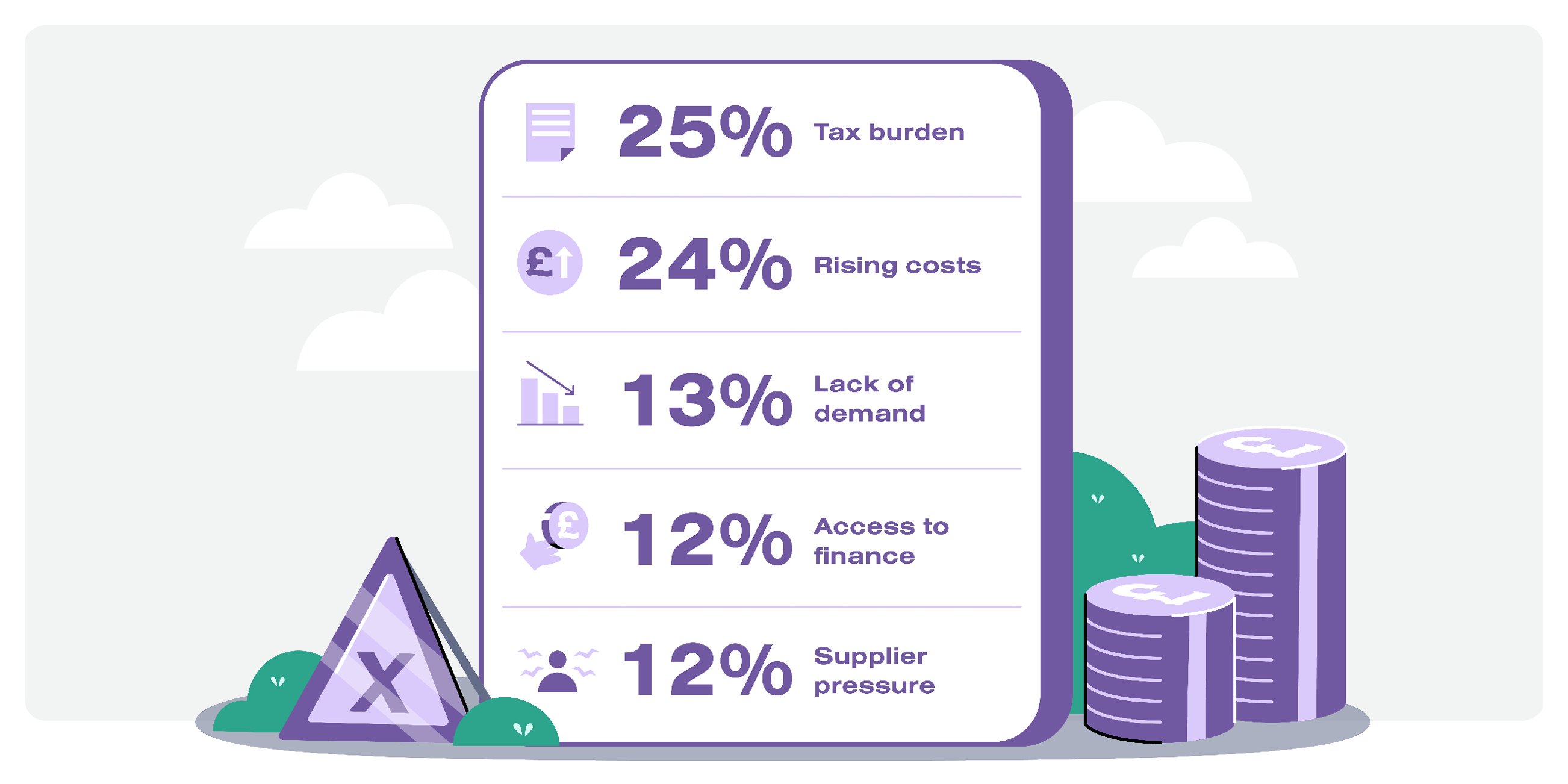

What's causing cash flow problems for UK SMEs?

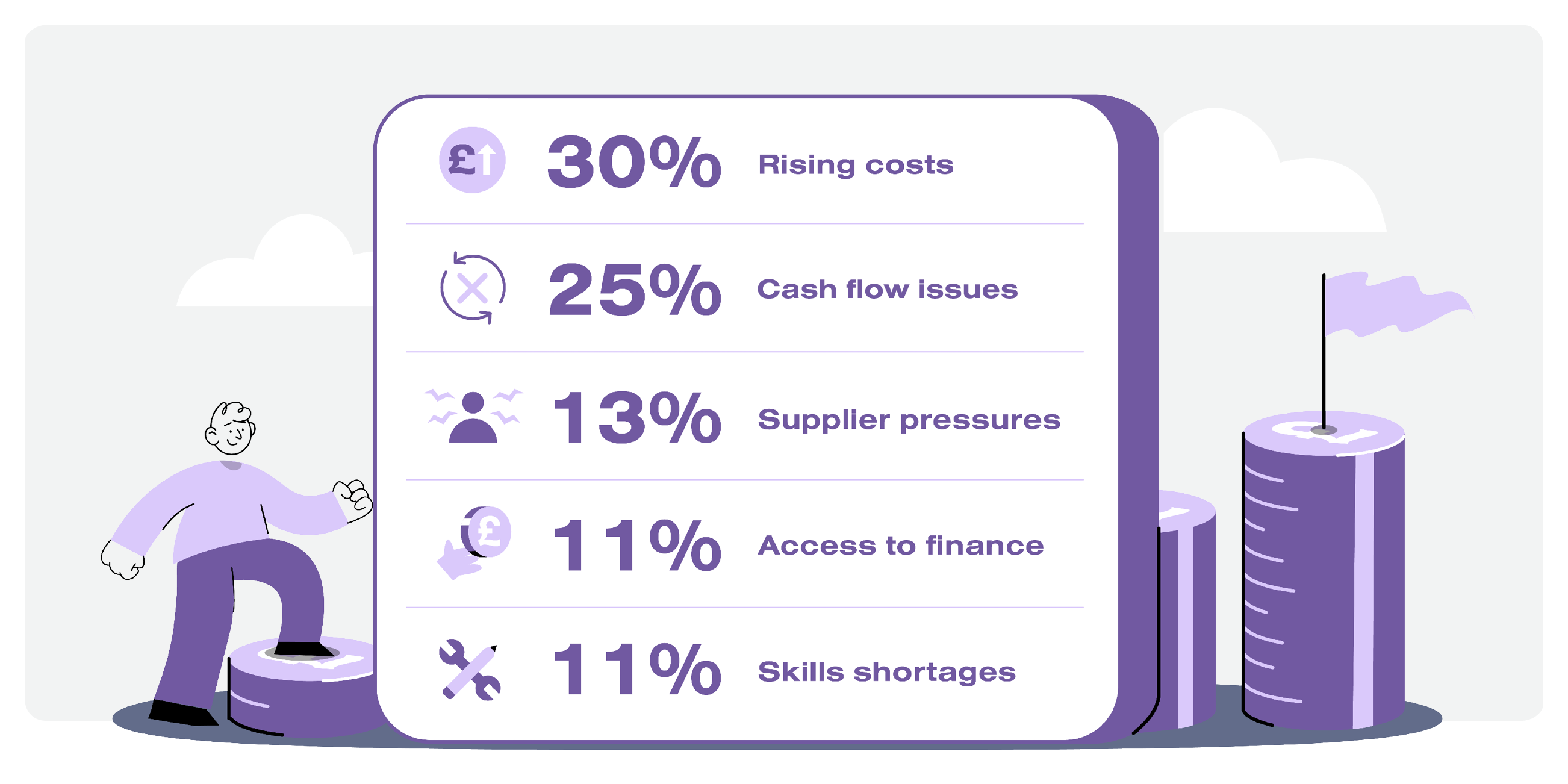

It's rarely just one thing. Our research found that 30% of SMEs named rising costs as their biggest challenge in 2025, while 25% pointed directly to cash flow issues. Add in supplier pressures (13%) and difficulties with access to finance for SMEs (11%), and you've got a perfect storm.

For hospitality businesses, it hit even harder - 56% said cash flow was their most significant barrier, which is more than 3 times higher than any other sector.

The root causes are well known: energy bills, wage increases following changes to the National Living Wage, higher Employers' National Insurance contributions, and suppliers passing on their own cost increases. Each one chips away at your available cash, leaving less room to manoeuvre.

How are rising costs pushing SMEs towards SME funding?

When cash is tight, businesses face a choice: wait it out or find a way to bridge the gap.

Our data shows that 24% of SMEs said supplier price increases or late payments would trigger them to seek SME funding. A further 14% would turn to external finance specifically to cover cash flow gaps, and 11% to handle tax obligations.

That's a significant proportion of UK businesses actively planning around the assumption that they'll need outside support, not because they're failing, but because the environment demands it.

In 2026, 71% of SMEs say they're likely to seek external finance. That's not a sign of struggle - it's a sign of smart planning.

Why are UK SMEs looking beyond traditional banks?

Banks still play a role, but they don't always move fast enough. Our research found that while 40% of SMEs used a bank or high-street lender in 2025, a growing proportion are turning to alternative lending options - particularly smaller businesses with revenues between £200k and £500k.

Speed and flexibility matter. When a supplier increases prices overnight, or a late payment leaves you short, you don't have weeks to wait for a decision.

27% of SME owners say digital or online application processes are their top priority when choosing a lender. A further 20% prioritise flexible repayment terms - finance that bends around your business, not the other way around.

That's exactly why alternative lenders like Lovey are becoming a go-to for business owners who need to move fast without the faff.

Here at Lovey, we are a business loan lender and broker, so we compare all the loan options for you in one place and find the best deal when it comes to loan amount, repayment terms and interest rates.

Got 60 seconds? That's all it takes to check how much you can borrow with Lovey.

The businesses that come out on top in a tough climate are the ones that plan. Waiting until your cash flow hits a wall before exploring SME lending options puts you on the back foot.

Our research found that 20% of SME owners say improving cash flow is their single biggest priority for 2026. The good news? There are more options available than ever - and applying doesn't have to be complicated.

Whether you're looking to cover a short-term gap, manage rising supplier costs, or give yourself the headroom to keep growing, SME funding UK options exist to help you do exactly that.

This article draws on findings from Lovey's 2026 H1 SME Finance Outlook report - a survey of 504 UK SME owners across retail, manufacturing, hospitality and construction, conducted between 2025 and 2026.

For the full data, including sector breakdowns, regional insights and borrowing behaviour, download the complete report.

Download the SME Finance Outlook report